Rising interest rates and recession fears continue to weigh on investors as the Consumer Price Index (CPI) report for August was stubbornly high at 8.3%. With rising interest rates impacting bond markets, most investors have seen both their equity and bond portfolios lose value. This environment may remain challenging until there is clarity on inflation as the Fed’s stance is firm that they intend to fight inflation regardless of the consequences to the U.S. economy.

Inflation metastasizes across the economy

Earlier this summer, inflation spiked to 9.1%, a 30-year high, ending a goldilocks period of low interest rates, contained inflation and steady growth. The initial spike in inflation was driven by surging demand for goods aided by stimulus payments to individuals, strong wage growth and rising commodity prices. Initially, inflation was believed to be transitory and due to supply chain congestion, but as higher prices spread into housing, services and wages, inflation has admittedly become more entrenched across the economy.

The Fed – higher rates

The Fed’s primary tool to combat inflation is raising interest rates which increases borrowing costs for consumers. Consumers who use credit will see higher costs to buy goods – especially more expensive items like homes and cars. The Fed anticipates that higher rates will lead consumers to reduce spending and slow aggregate demand which will help to cool out-of-control inflation. One input, pending home sales for July were down -22.5% year over year as higher interest rates sharply reduced home affordability.

Reducing inflation will take time

As Tuesday’s August CPI showed, the Fed’s battle against inflation will take time. There are three main reasons why we expect inflation to remain stubbornly high:

- The U.S. consumer is healthy. Low debt service ratios, soaring prices for houses, rising wages and generous stimulus payments have helped consumers’ balance sheets and bolstered spending. So far, higher interest rates have had little effect on the U.S. consumer who continues to drive GDP growth.

- Sticky components of inflation are high. Inflation has spread into areas of the economy where prices are slow to change like services, wages, and housing. In particular, shelter prices (rents) have followed soaring home prices. Shelter is an important component of CPI (32%) and core CPI (40%). In August’s CPI report, shelter prices increased 6.3% year over year, rising at the fastest rate since 1991. Over the past 20 years shelter has helped to anchor low inflation, now shelter is doing the opposite.

- Tight labor markets. With the U.S. economy running at or near full employment of 3.7% and with job openings at 2x the number of unemployed persons, labor markets are the tightest in post WWII history. It will be challenging for the Fed to slow the economy enough to create the slack needed in the labor markets to cool wage growth. There are some signs that workers who may have left the workforce due to the pandemic are returning to work, but the labor market remains very tight.

Typically, actions by the Federal Reserve take 3-6 months to have an impact on the economy, so we expect to see demand gradually decline as consumers feel an increasing impact of higher interest rates. We expect the Fed to continue to raise interest rates until they see sustained signs of lower prices and some slack in labor markets. The August CPI number highlights that the Fed has a long way to go to tame inflation.

Recession fears

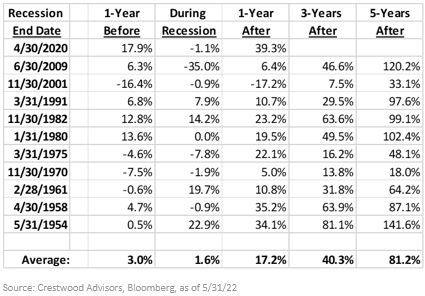

Our base case remains that U.S. economic growth continues to slow but remains positive year over year. Considering economists estimate the long-term growth rate of the U.S. economy to be 1.0%-2.5%, the chance a slowdown dips the economy into a recession is higher than normal. Importantly, a deep recession similar to the Global Financial Crises in 2008/2009 is unlikely. Consumers remain in great financial shape with lower debt service and higher household wealth. Similarly, banks who sailed through the pandemic are much better prepared for any downturn. We expect any recession would be a shallow one.

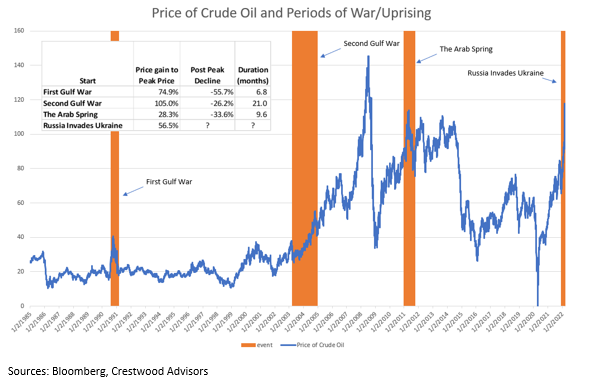

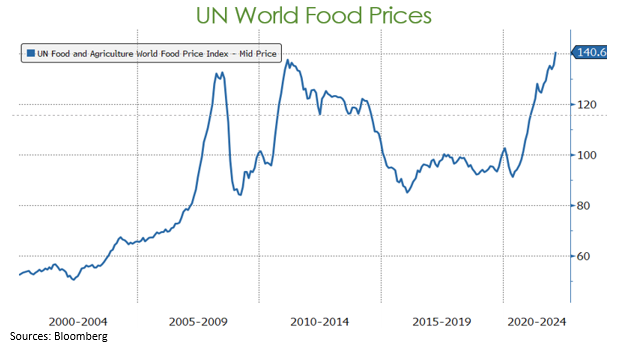

Russia rankles Europe

In response to sanctions for their invasion of Ukraine, Russia has sharply restricted natural gas flowing to Europe. Germany is particularly vulnerable as before the war 55% of Germany’s consumption of natural gas came from Russia. In anticipation of higher winter demands, Germany has been building natural gas storage, curtailing consumption, and switching to other sources for electrical generation. Uncertainty runs high as no one can predict Russia’s actions, but a prolonged shutoff could affect GDP growth as gas will need to be rationed.

Positioning

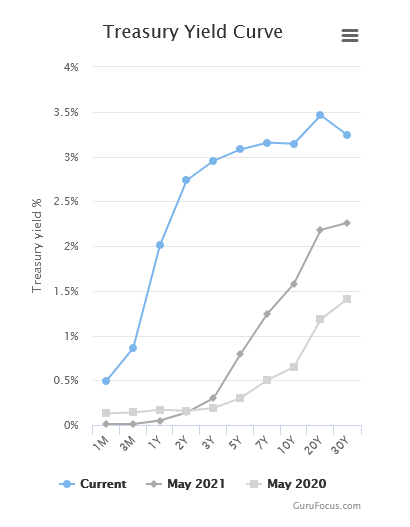

We continue to focus on quality for both fixed income and equity investments. For fixed income investors, we have built an allocation to short-duration, high-quality bonds to protect from rising interest rates and credit concerns. Shortening duration has been important to help offset falling prices as interest rates have risen sharply this year. Investors have favored high quality bonds over lower quality bonds as slowing economic growth and higher borrowing costs may stress some issuers.

In the U.S. stock market, we remain focused on quality companies with solid growth prospects. Earnings growth has been solid as the S&P 500 index posted 6.2% earnings growth in the second quarter. With the S&P 500 down -16.1% YTD, market valuations have improved dramatically. The below chart shows the forward price to earnings multiple (a measure of how much stocks cost), has fallen from 22.8x at the beginning of the year to 17.4 which is just below the 10-year average of 17.8.

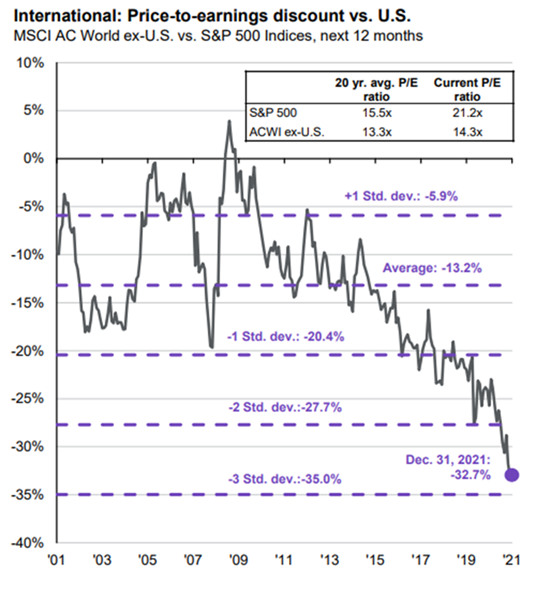

We remain underweight international equities and defensively positioned in European equities. Though the energy crisis and war in Ukraine are concerns, European earnings have held up relatively well and are helped by the U.S. Dollar strength.

We continue to be patient and opportunistic as we evaluate companies and make portfolio adjustments. To that end, we have added several new investments in strong businesses that now offer compelling valuations. Additionally, your position in short term bonds, including U.S. Treasuries, offers an attractive yield, high degree of safety and a source of potential liquidity. Finally, while incurring losses is never our goal, the volatility & weakness throughout 2022 has provided us opportunities to focus on new opportunities and tax-loss harvesting across taxable portfolios.

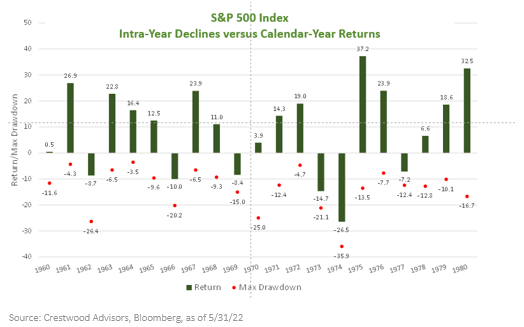

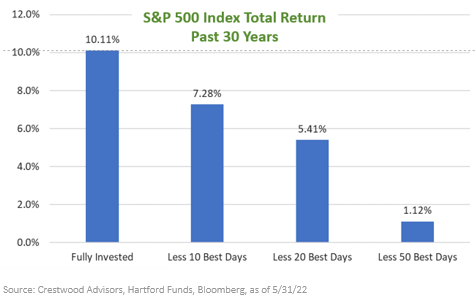

Times like these are never easy as an investor; however, historically, these volatile periods present opportunities to long term investors. As always, we caution against reacting to short-term volatility and encourage sticking with well-considered, long-term investment plans.