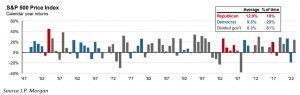

2023 Consensus Forecasts – A Big Miss:

At the beginning of last year, 85% of economists forecasted a recession for the U.S. as many indicators, including an inverted yield curve, were flashing red.

Throughout 2023, the U.S. economy not only avoided a recession, but growth accelerated in the 3rd quarter to a robust rate of 4.9%. Low unemployment and strong wage growth helped consumers shrug off higher interest rates and continue spending.

The best news from last year was that inflation continued to trend lower toward the Fed’s target of 2.0%, falling to 3.1%, even with strong economic growth. At the December Federal Reserve meeting the Fed indicated that interest rates have peaked for this cycle, shifting their focus to maintaining current growth.

Resilient U.S. Economy Continues:

This time last year, we were more optimistic than consensus forecasts because we believed consumer spending was less sensitive to interest rate increases than in past cycles. Today, we believe that the forces affecting 2023’s growth are still in place for 2024.

Economists have underestimated two trends. First, more stable service sectors have come to dominate the U.S. economy. Second, consumers are locked into low interest rates mortgages which have helped shield them from the Fed’s 11 interest rate hikes.

The U.S. economy is a service economy. In 1970, consumption of services surpassed that of goods. Today, 80% of jobs in America are service jobs in industries like business services, health care, governments, and leisure. Spending on services tends to be more recession-resistant and helps to stabilize GDP growth. Conversely, spending on goods tends to decline during recessions and sometimes the declines have been steep. During the Global Financial crisis in 2009, the consumption of goods fell -6.8%, while consumption of services fell only -1%.

Today, the strength in the U.S. economy is focused on these service sectors, driving wage growth, consumption and, in turn, contributing to inflation.

Implications: As the U.S. economy evolves and becomes more service-oriented, we should expect more consistent growth and less severe recessions. Tightness in labor markets, especially in service areas, suggests inflation may be slower to come down than many expect. As a result, it could take longer than expected to reach the Fed’s target of 2.0%.

Consumers have less variable-rate debt. Compared to prior economic cycles, higher interest rates have had less of an effect on consumer spending. In prior cycles, higher borrowing costs pinched consumers who had credit card debt or variable-rate mortgages. Today, it is estimated that 82% of mortgage holders have a mortgage rate below 5% and most of those loans are fixed rate. Also, many consumers used the pandemic stimulus payments to reduce credit card debt, so consumer finances have been excellent and supported spending growth despite higher interest rates.

Implications: Consumer spending will remain healthy as higher rates pinch consumers less due to changes in consumer debt. We expect housing markets will remain tight as many current homeowners are reluctant to transact if their house has a low-interest mortgage. Considering consumers are somewhat interest rate immune, we expect rates to remain elevated for the foreseeable future.

Soft Landing Likely in 2024

Crestwood’s 2024 outlook for economic growth is positive. We expect consumer spending to remain healthy considering the durability of the service economy and consumer rate insensitivity. Combined with tight labor markets and solid wage growth, we remain optimistic that the backdrop for markets is supportive.

Since 1960, the Fed has achieved only one economic soft landing, where higher interest rates slowed the economy without an ensuing recession. 2024 is shaping up to be the second soft landing. We are encouraged by the Fed’s comments that they are pleased with progress on containing inflation. Rates have likely peaked and appear poised to decrease in 2024.

Still, we expect this ride to be bumpy as inflation will remain sticky and slow to fall.

What could delay or derail the path forward:

- Global geopolitical recession. Ian Bremmer of the Eurasia Group believes we are in a geopolitical recession which is like an economic recession except it affects many countries and lasts longer. With the outbreak of war in the Middle East, the ongoing war in Ukraine and the U.S. struggling with political dysfunction, geopolitical good news may be hard to find in 2024. While the U.S. economy is largely unaffected by these conflicts, the humanitarian toll on civilians and soldiers in these regions is staggering and tragic.

- Rates stay higher for longer. Even though the cost of debt has fallen recently, higher rates could be a risk, affecting low-end consumers and highly leveraged companies that need refinancing. Higher defaults could stress non-bank lenders who have experienced rapid growth and face little regulation.

- Commercial office real estate is facing significant headwinds. Falling demand and increased supply are the result of a restructuring of the modern workforce to a mix of in-office, hybrid and fully remote workers. The market adjustment in office prices will likely be significant and take years to unfold. Sizable nonperforming real estate loans have yet to materialize. If they do, losses could affect banks’ balance sheets and force them to reduce lending. Small banks are particularly exposed as 44% of their assets are commercial real estate loans.

- China is a source of uncertainty. China’s growth model that focuses on exports and infrastructure investment has reached its limits and efforts to support domestic consumption need to be expanded. Elevated debt burdens and falling real estate prices will continue to affect consumer spending and growth. International investors are frustrated with the decline of legal protections for shareholders and increased government intervention.

Market Outlook: Optimistic Backdrop

With a positive economic backdrop, we expect 2024 to bring continued modest growth and opportunities in financial markets. Federal Reserve commentary has become less restrictive and more positive for markets.

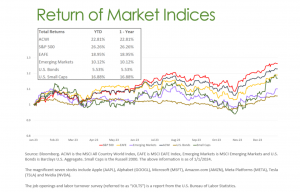

For equity markets, the positive economic backdrop should support continued revenue and earnings growth. All eyes will be on the Magnificent Seven stocks – Apple, Microsoft, Alphabet, Tesla, Meta, Amazon and Nvidia – to see if they can sustain their fundamentals and valuation. These companies are huge, with their combined market capitalization totaling over 30% of the S&P 500 Index which is equivalent to the value of all the stocks trading in Canada, France, China, UK and Japan!

In 2023, the magnificent seven were up a combined 107% and accounted for 60% of the gain in the S&P 500 index. Should investor sentiment sour on these companies, the S&P 500 index will struggle. For individual equities, we remain focused on quality investments which we believe outperform over a market cycle with lower volatility.

For bond markets, after decades of low interest rates, we believe higher yields – around 4% – will provide attractive returns for fixed-income investors. We believe the Fed’s December pivot towards lowering interest rates gives investors a solid backdrop to investing in fixed income. Investors should be rewarded by extending maturities and locking in attractive interest rates.

As always, we view all market forecasts with skepticism and keep a close eye on economic data and markets. Considering forecasters’ big miss for 2023, it is important to be flexible in our views and remain focused on improving long-term outcomes for client portfolios.

This document is provided for general informational purposes only and should not be construed as containing investment advice. For individualized investment advice, please consult your adviser. This document contains forward-looking statements, predictions and forecasts (“forward-looking statements”) concerning our beliefs and opinions in respect of the future. Forward-looking statements necessarily involve risks and uncertainties, and undue reliance should not be placed on them. There can be no assurance that forward-looking statements will prove to be accurate, and actual results and future events could differ materially from those anticipated in such statements.