Webinar: Behavioral Investing – Overcoming Biases for Better Decision Making

January set a tone for a more cautious investor stance. Much of the U.S. was forced to trudge through snow from recent winter storms and similarly labor markets are trudging slowly along. We remain in a low-hire, low-fire equilibrium. Employers are hesitant to expand, given fiscal uncertainty but are equally loath to let go of trained staff.

While corporate earnings are projected to remain healthy, with an estimated 14% growth for the year, the variables of trade policy and central bank transition create a challenging environment.

After three consecutive cuts to end 2025, the Fed shifted stance to a wait-and-see outlook as the committee voted to hold interest rates steady at the January meeting. The FOMC’s internal debate appears centered on the neutral rate (the level at which policy neither stimulates nor restricts growth) with two of the twelve voters advocating for further cuts to support a slowing manufacturing sector.

A notable development was the nomination of Kevin Warsh to succeed Powell when his term ends in May. During his previous time as a Fed Governor (2006-2011), Warsh was initially supportive of crisis-era liquidity and low rates but opposed the second round of quantitative easing (QE2) in 2011 which he believed would lead to inflation.

Warsh has yet to be confirmed, which could be a challenging process1, but understanding his outlook on the Federal Reserve can provide insight to how he might act as Fed Chair.

Warsh In His Own Words

In a November opinion piece in the Wall Street Journal2, Warsh outlined his vision:

“Fundamental reform of monetary and regulatory policy would unlock the benefits of AI to all Americans. The economy would be stronger. Living standards would be higher. Inflation would fall further. And the Fed will have contributed to a new golden age.”

Setting aside the utopian prose, his outlook is reflected in four theses, and we examine each in the context of what they mean for investors.

1) “The Fed should discard its forecast of stagflation in the next couple of years”. He believes that ”AI will be a significant disinflationary force, increasing productivity and bolstering American competitiveness. Productivity improvements should drive significant increase in real take-home wages.”

Translation: The Fed has been driving by looking in the rear-view mirror (backward looking data that shows a slowing economy and sluggish labor market). Future productivity growth and lower inflation from AI isn’t being factored in, so the Fed is being too conservative.

Implications for Investors:

2) “Inflation is a choice.”

Translation: Warsh argues that inflation isn’t the product of an overheated economy but rather the result of too much government spending and expansion of the Fed’s balance sheet. The head of the snake (the Fed) would be eating less of its own tail (buying its own debt).

Implications for Investors:

3) “The Fed’s rules and regulations have systematically disadvantaged small and medium-sized banks, which has slowed the flow of credit”.

Translation: Warsh believes that by easing regulatory requirements for smaller lenders, there will be additional availability of credit.

Implications for Investors:

3) “Fed leaders have tried to bind U.S. banks to a complicated, vaunted set of rules in the name of global regulatory convergence.”

Translation:

Warsh argues that the Fed should seek to deregulate U.S. banks and encourage them to de-couple rather than coordinate with their overseas counterparts.

Implications for Investors:

Capital Markets

Equity markets saw a notable rotation in January as investors grew cautious of the AI theme driving market recent gains amidst higher valuations. Notably this led to a wider breadth of stocks driving market gains including smaller companies (as measured by the Russell 2000).

Official data reported in January remains cloudy due to the late-2025 government shutdown. This data lag created a volatility vacuum where anecdotal evidence and earnings calls carried more weight than usual as earnings were released.

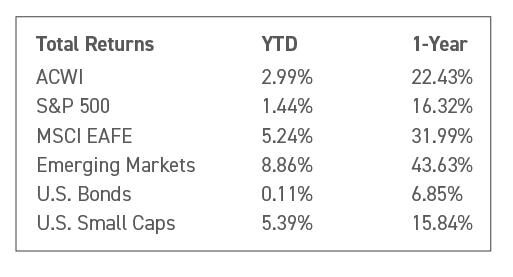

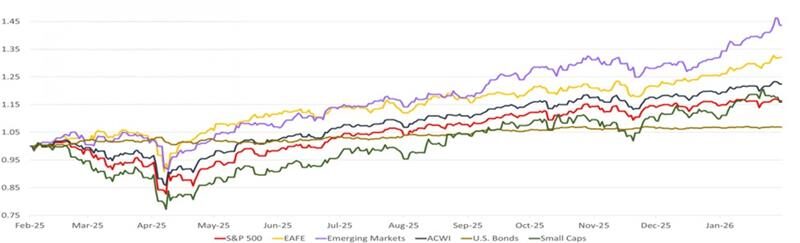

Emerging Market Equities lead the way returning an impressive 8.9% for the month. U.S. Small Caps (Russell 2000) and Developed International Equities (MSCI EAFE) also showed large gains, returning 5.4% and 5.2% respectively. U.S. Large Caps (S&P 500) lagged, returning 1.44% in January. Bonds, as measured by Bloomberg’s U.S. Aggregate index, were nearly flat for another month, eking out a slightly positive 0.11%.

Return of Market Indices

2025 was a year of economic uncertainty and concern, but also of resilience and growth. In this month’s Economic Update, we look back at the issues that dominated our thinking on the economy and financial markets each quarter and then look forward to what we’re focused on in 2026.

Source: Bloomberg. EAFE is MSCI EAFE Index(1), Emerging Markets is MSCI Emerging Markets(2) and U.S. Bonds is Barclays U.S. Aggregate(3). ACWI is the MSCI ACWI Index(4). Small Caps is the Russell 2000 Index(5). S&P 500 is the S&P 500 Index(6). The above information is as of 1/31/2026.

1 Warsh’s journey to become Fed Chair is unlikely to be quick. Post-nomination, the next step toward approval is for vetting to go through the Senate Banking Committee. However, committee member Senator Thom Tillis (R-NC) has indicated he would not on any Fed nominee until the Department of Justice’s investigation of Chair Powell over the Fed’s headquarters is resolved which he believes is politically motivated Senator Tillis’ term ends in 2026, and he is not seeking re-election, making him less susceptible to political pressure. The Senate Banking Committee is narrowly divided (13 Republicans to 11 Democrats), thus if Tillis refuses to support the nominee, the committee the nomination could stall.

2 Warsh, Kevin The Federal Reserve’s Broken Leadership, Wall Street Journal Opinion 11/16/25

This document contains forward-looking statements, predictions and forecasts (“forward-looking statements”) concerning our beliefs and opinions in respect of the future. Forward-looking statements necessarily involve risks and uncertainties, and undue reliance should not be placed on them. There can be no assurance that forward-looking statements will prove to be accurate, and actual results and future events could differ materially from those anticipated in such statements.

When we think about the financial decisions we make, we like to believe they’re always rational. Spend less. Save more. Invest wisely. In practice, however, emotions, habits, and social influences often play a quieter but equally powerful role.

You may find yourself maintaining a long-standing vacation routine even though your family’s schedule and interests have shifted. You might delay replacing a vehicle while weighing timing, tax considerations, or resale value. Or perhaps you’re evaluating a significant discretionary purchase after seeing peers make similar upgrades. None of these choices are inherently wrong, but they are worth considering.

Self-awareness helps surface the behavioral forces behind financial decisions. Familiarity, loss aversion, and social influence can subtly shape outcomes. When recognized, these dynamics become tools rather than blind spots, allowing you to make choices that better align with your broader financial picture and long-term priorities.

Below are several approaches designed to complement the way successful families already evaluate complex decisions.

Thoughtful Approaches to High-Quality Financial Decisions

Create distance before committing.

Significant decisions benefit from space. Allowing time between intention and execution, whether days or weeks, can surface considerations around timing, liquidity, taxes, and opportunity cost that are easy to overlook in the moment.

Clarify the objective.

Before proceeding, articulate what the decision is meant to accomplish, enhancing lifestyle, simplifying complexity, supporting family priorities, or responding to external signals. Precision around purpose sharpens judgment.

Evaluate the full context.

Consider the choice alongside your broader financial architecture: balance sheet strength, upcoming liquidity needs, investment strategy, estate planning priorities, and philanthropic objectives. Strong decisions rarely exist in isolation.

Stress-test the alternatives.

Examine credible paths rather than defaulting to a single course of action. What changes if you act now versus later? Do you allocate capital here versus elsewhere? A structured comparison often strengthens conviction.

Preserve intentional flexibility.

Well-designed financial lives include room for enjoyment and spontaneity, within a framework that protects what matters most. Defining that flexibility in advance allows decisions to feel confident rather than reactive.

We are hard-wired to respond emotionally, and opportunities to act are constant. When faced with a meaningful financial choice, pausing to ask, “How does this fit within my broader plan?” can materially change the outcome.

At Crestwood, we help families connect day-to-day decisions to long-term purpose through a comprehensive planning process that integrates investment strategy, tax efficiency, estate considerations, and philanthropy. If you would like to explore how behavioral insights fit within your own roadmap, your Crestwood team is always available to serve as a thoughtful sounding board.

This document is provided for general informational purposes only by Crestwood Advisors, an investment adviser. Crestwood Advisors does not endorse, sponsor, or promote any of the products or companies listed or mentioned in this material. Any references to specific products or services are purely incidental and are included solely to illustrate potential strategies or concepts. The inclusion of such references does not imply any form of partnership, relationship, or approval by the Firm.

As we move into 2026, retirement savers are facing important rule changes in employer plans like 401(k), 403(b), and 457(b) accounts. These changes affect base contribution limits, “catch-up” contribution limits for those over 50 and between the ages of 60-63, and the tax treatment of “catch-up” contributions for higher-income savers.

Key 401(k) Changes for 2026

The Limit for Base 401(k) Contributions Rises

For 2026, the maximum elective deferral, the amount an employee can contribute from their salary to a 401(k) plan, increases to $24,500, up from $23,500 in 2025. This adjustment reflects inflation and gives savers more room to build their nest eggs each year. Note: this change applies to contributors regardless of age.

Catch-Up Contributions Rise for Older Savers

So-called “catch-up” contributions, additional amounts that older savers can put aside beyond the standard limits, are also rising in 2026. These enhanced catch-up limits are designed to help those closer to retirement age accelerate savings, especially if they started late or temporarily paused contributions in the past.

Catch-Up Contributions Must Be Roth for High Earners

Perhaps the most significant shift for 2026 impacts how catch-up contributions are taxed.

Note that your 401(k) plan must offer a Roth option for these contributions to take place. If your 401(k) doesn’t have a Roth feature, you might not be able to make catch-up contributions at all under the new rule. Check with your HR or plan administrator about whether your plan supports Roth contributions and, if not, whether it plans to add them.

Keeping Pace with the New Rules

By knowing the rules and planning ahead, you can make smarter decisions about when and how to save. The right moves in 2026 can help you grow your retirement nest egg while managing your tax bill and securing a more predictable income stream for later years.

If you’re unsure about how the new rules will impact your financial plan, please consult with a Crestwood financial advisor or tax professional.

Internal Revenue Service. “401(k) Limit Increases to $24,500 for 2026, IRA Limit Increases to $7,500.” IRS, 13 Nov. 2025, www.irs.gov/newsroom/401k-limit-increases-to-24500-for-2026-ira-limit-increases-to-7500

The legacy you leave behind should not be defined solely by the sum total of your estate, but by the goals, values, and purpose that shape how your wealth is created, managed, and transferred, your “why.” Strategic planning, when informed by your intentions, provides a powerful framework for crafting your legacy.

Be Intentional

Creating a strategy for your legacy begins with clarity of purpose. Before technical tools and legal structures are put in place, you must first define what you want your wealth to represent. Core values such as responsibility, generosity, independence, education, and service often shape these intentions. When planning is aligned with these principles, financial decisions gain coherence and direction. This alignment also helps ensure that wealth is not distributed arbitrarily, but intentionally, in a way that reflects both your personal beliefs and long-term goals.

Every decision in strategic planning, how your assets are structured and invested, when they are transferred, and to whom or to what, defines your priorities. When these decisions are motivated by your core values, your wealth becomes a narrative rather than just numbers on a statement. Your plan will tell a story about what matters to you, what you believe, and what you encourage future generations to embody, and that story translates into effective legal, financial, and philanthropic structures to ensure your values and intentions endure across time.

Learn how to invest with intention and continue working towards your legacy goals, even when markets are volatile.

Behavioral Investing: Overcoming Biases for Better Decision Making

February 12, 2026

12:00 pm – 1:00 pm ET

Register Now

Prepare the Next Generation.

Succession planning is essential for ensuring continuity, particularly in families with closely held businesses or significant shared assets. Effective succession planning goes beyond defining heirs and key roles, it involves preparing the next generation to manage wealth and business interests, in alignment with the family’s values and intentions. This may include defining leadership roles, establishing governance structures, and providing education or mentorship. By doing so, individuals can reduce the risk of conflict, mismanagement, or dissipation of wealth. Succession planning ensures that assets are not only transferred but entrusted with clear expectations and a shared sense of purpose.

Support Your Values.

Charitable giving offers one of the most direct ways to align wealth with values. Philanthropy allows you to support causes that reflect your beliefs, passions, and vision for a better future. Whether focused on education, healthcare, faith-based initiatives, social equity, or environmental conservation, charitable giving transforms wealth into a force for positive change.

Strategic charitable planning also enables you to give in ways that are sustainable and impactful over time. Charitable trusts, donor-advised funds, and family foundations can provide structure and continuity, allowing charitable intentions to endure beyond a single lifetime. In this way, philanthropy becomes not just an act of generosity but a defining element of your legacy.

Lifetime Gifting.

Gifting is another powerful strategy for both preserving wealth and expressing what is meaningful to you. By transferring assets to family members during your lifetime, you can reduce the size of your taxable estate while directly supporting the development and well-being of your loved ones.

More importantly, gifting provides an opportunity to model your values in action. Thoughtful gifts can be used to encourage education, entrepreneurship, or responsible financial behavior. When paired with open communication, gifting can reinforce lessons about stewardship, gratitude, and accountability. Rather than creating entitlement, values-driven gifting helps cultivate independence and purpose, ensuring that wealth serves as a foundation for growth rather than a source of complacency.

Estate Tax Mitigation.

Tax efficiency is a critical component of preserving wealth and honoring your intentions. Taxes can significantly erode an estate, reducing the resources available to support family members or philanthropic goals.

Estate tax mitigation strategies seek to minimize unnecessary tax exposure through techniques such as leveraging exemptions, utilizing trusts, and timing asset transfers appropriately to help ensure that more wealth is preserved for its intended purposes.

Guide Your Legacy.

Strategic planning guided by core values and clear intentions can play a key role in shaping the legacy you leave behind. Such strategies allow wealth to serve not only as financial security, but as a lasting expression of your purpose, responsibility, and vision. In the end, a well-planned legacy is not measured by the numbers you see on a statement, but by how faithfully it carries forward the values that give it meaning. As you look ahead to the coming year and beyond, think about the steps you can take to ensure that your legacy is the one you intend.

If you would like support in helping you plan for your legacy, your Crestwood team is here to help you move into the next stage with confidence.

2025 was a year of economic uncertainty and concern, but also of resilience and growth. In this month’s Economic Update, we look back at the issues that dominated our thinking on the economy and financial markets each quarter and then look forward to what we’re focused on in 2026.

Q1: Fear of the Unknown

As the Trump administration in Washington found its footing, expectations for global trade reform loomed large. In Q1, our attention was on the impact that tariffs could have on inflation and economic growth, and how the unpredictability of outcomes could spook the financial markets.

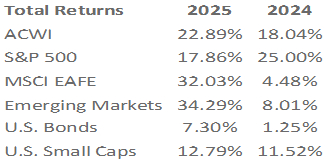

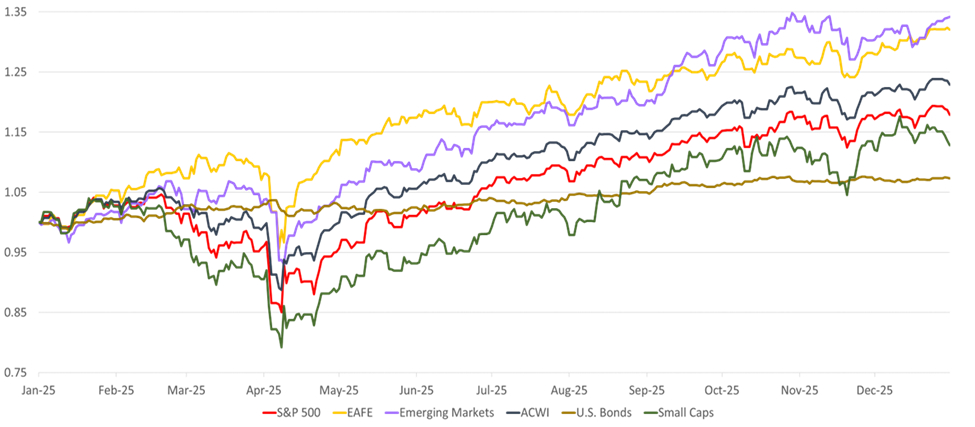

A reactionary massive surge in imports contributed to a contraction in GDP of 0.5% in quarter1. At the same time, inflation remained elevated, leading the Fed to keep its restrictive monetary policy in place. In this uncertain environment, the US stock market struggled for direction as investors feared that recession, or even stagflation, might be on the horizon. By quarter’s end, volatility had returned to the market, and the S&P 500 had lost 4.3%.

In our March update, we reminded investors of the resilience of American institutions and advised them to remain patient, focusing on long-term goals rather than short-term volatility. This advice would serve them especially well in the quarter to come.

Q2: Liberation Day Selloff and Recovery

The second quarter began with the Liberation Day announcement of sweeping tariffs on America’s trading partners. The size and scope of the tariffs caught investors off guard, resulting in a swift selloff across equity markets, including an 11% decline in the S&P 500.

We pointed out that periods of extreme uncertainty may persist for a time, but they are not permanent, and that markets react favorably once a measure of predictability returns.

The announcement of a three-month “pause” in the tariff rollout signaled such a window of predictability. By the end of the quarter, equity markets had recovered, and the S&P was up nearly 6% YTD.

Q3: Shooting the Messenger and Divergence at the Fed

Tariff risk persisted into the third quarter; however, delayed implementation timelines and constructive progress in trade negotiations helped ease market concerns. In Q3, the Bureau of Labor Statistics revised estimates on job growth downward. The reaction was swift: President Trump fired the head of the BLS, the dollar weakened, and equity markets declined. Though the Fed was divided on the pace of rate cuts, the slowing economic data proved enough to convince them to cut rates by 0.25% in September. Equity markets responded favorably, with the S&P 500 rising by a healthy 7.8% in the quarter.

Q4: Closing Time and K-Shaped Data

The fourth quarter began with the shutdown of the Federal government. While every shutdown is unique, we expected the impact on equities to be modest and temporary, and recommended clients stay the course rather than trading on this news. This was indeed sound advice. Despite becoming the longest shutdown on record, the impact on equity markets was mild.

As economic growth took center stage toward year-end, we brought attention to the distinctive nature of the current K-shaped data, which evidenced a bifurcated mix of “winners and losers” in equity markets, higher vs. lower-income households, and other areas of the economy.

The fourth quarter was a victor lap for patient equity investors. The government reopened, and the Fed committed to a “normalization” path with 0.25% rate cuts in October and December.

Looking Ahead: 2026 Rhymes, but will not Repeat

We believe three trends will play out in 2026:

The combination of these three trends points toward a favorable backdrop for investors in 2026. However, we continue to recommend a diversified and flexible portfolio philosophy, rather than chasing last year’s “winners” and shunning last year’s “losers.”

No one could have predicted the events of 2025 that we recapped above, but veteran investors know that every new year holds unexpected twists. As we noted many times throughout 2025, the best maxim for long-term investment success is “Patience and Discipline.”

Capital Markets

December was a soft month for US investment returns, while overseas equities saw an appreciable rise. The All-Country World Equity Index (ACWI) rose 1%. Both Developed Non-US equities, as measured by the EAFE and Emerging Market Equities, as measured by the MSCI EM Equity Index, rose by 3%. The S&P 500 finished nearly flat for the second month in a row (+0.1%). Likewise, bonds as measured by Bloomberg’s US Aggregate index were nearly flat, declining by 0.2%. US Small Caps declined 0.6% for the month.

Source: Bloomberg. EAFE is MSCI EAFE Index(1), Emerging Markets is MSCI Emerging Markets(2) and U.S. Bonds is Barclays U.S. Aggregate(3). ACWI is the MSCI ACWI Index(4). Small Caps is the Russell 2000 Index(5). S&P 500 is the S&P 500 Index(6). The above information is as of 12/31/2025.

1 Since GDP is a measure of domestic production, imports represent foreign 2 production and thus are subtracted from the GDP calculation as these are already accounted for in domestic spending.

2 Source: FactSet Earnings Insight 12/19/25

3 The Magnificent 7 currently include Nvidia, Apple, Microsoft, Amazon, Alphabet (Google), Meta (Facebook), and Tesla. While Broadcom replaced Tesla as one of the 7 largest stocks in the S&P 500 by market capitalization, Tesla is still commonly included in the Mag 7 group.

This document contains forward-looking statements, predictions and forecasts (“forward-looking statements”) concerning our beliefs and opinions in respect of the future. Forward-looking statements necessarily involve risks and uncertainties, and undue reliance should not be placed on them. There can be no assurance that forward-looking statements will prove to be accurate, and actual results and future events could differ materially from those anticipated in such statements.

Required Minimum Distributions – commonly called RMDs – are mandatory withdrawals from certain tax-advantaged retirement accounts. The IRS requires RMDs because these accounts were funded with pre-tax dollars, and taxes were deferred until money is withdrawn. RMDs ensure that the government eventually collects income tax on those savings.

Understanding the rules surrounding Required Minimum Distributions (RMDs) and knowing exactly when you must begin taking them is essential for optimized tax planning, including avoiding stiff tax penalties on your savings. Recent law changes have shifted the starting age for RMDs, making it more important than ever to stay informed so you don’t miss key deadlines.

What Accounts Require Minimum Distributions?

RMDs generally apply to the following accounts:

Roth IRAs do not require RMDs during the owner’s lifetime, though inherited Roth IRAs do have rules for beneficiaries.

The Current Rules for RMDs

The One Big Beautiful Bill Act, commonly referred to as the OBBBA, passed in 2025, made significant changes to tax law. However, it did not impact laws relating to RMDs.

Rather, the latest rules for RMDs have been set out in the SECURE Act 2.0, which became law on December 29, 2022. And even though penalties for not taking RMDs have been reduced, they are still severe, so it’s important to keep track of your personal time frame.

The current key provisions for RMDs include the following:

RMD Starting Age

Your first RMD must be taken the year you turn:

Most seniors today will begin RMDs at age 73.

For your very first RMD, you may choose one of two options:

The Penalties for Not Taking RMDs on time

The IRS penalty for missing all or part of an RMD used to be 50% of the amount not withdrawn. Today, the penalty is:

How Much and For How Long

Once you begin taking RMDs, you must continue taking them each year until your tax-deferred savings are exhausted. The minimum amount you are required to take each year is calculated based on:

The calculation basically divides your account balance by the number of years you are expected to live to get an annual distribution amount. Your financial institution can calculate the RMD for you, but it is ultimately your responsibility to ensure the correct amount is withdrawn on time.

Plan Ahead

Avoiding stiff penalties from the IRS is a strong incentive to make sure you take your RMDs on time. But it’s also advisable to plan ahead in managing your distributions so that they fit within your broader framework for taxable income levels as well as your overall retirement and estate plans.

If you would like to learn more about RMDs, please reach out to your Crestwood team. If you are not yet working with Crestwood, please contact us to discuss your individual circumstances.

This document is provided for general informational purposes only by Crestwood Advisors, an investment adviser. Crestwood Advisors does not provide legal advice, and this document should not be construed as containing legal advice. For legal advice, consult with a licensed attorney. This document should not be construed as containing tax advice. For tax advice, consult with your tax adviser.

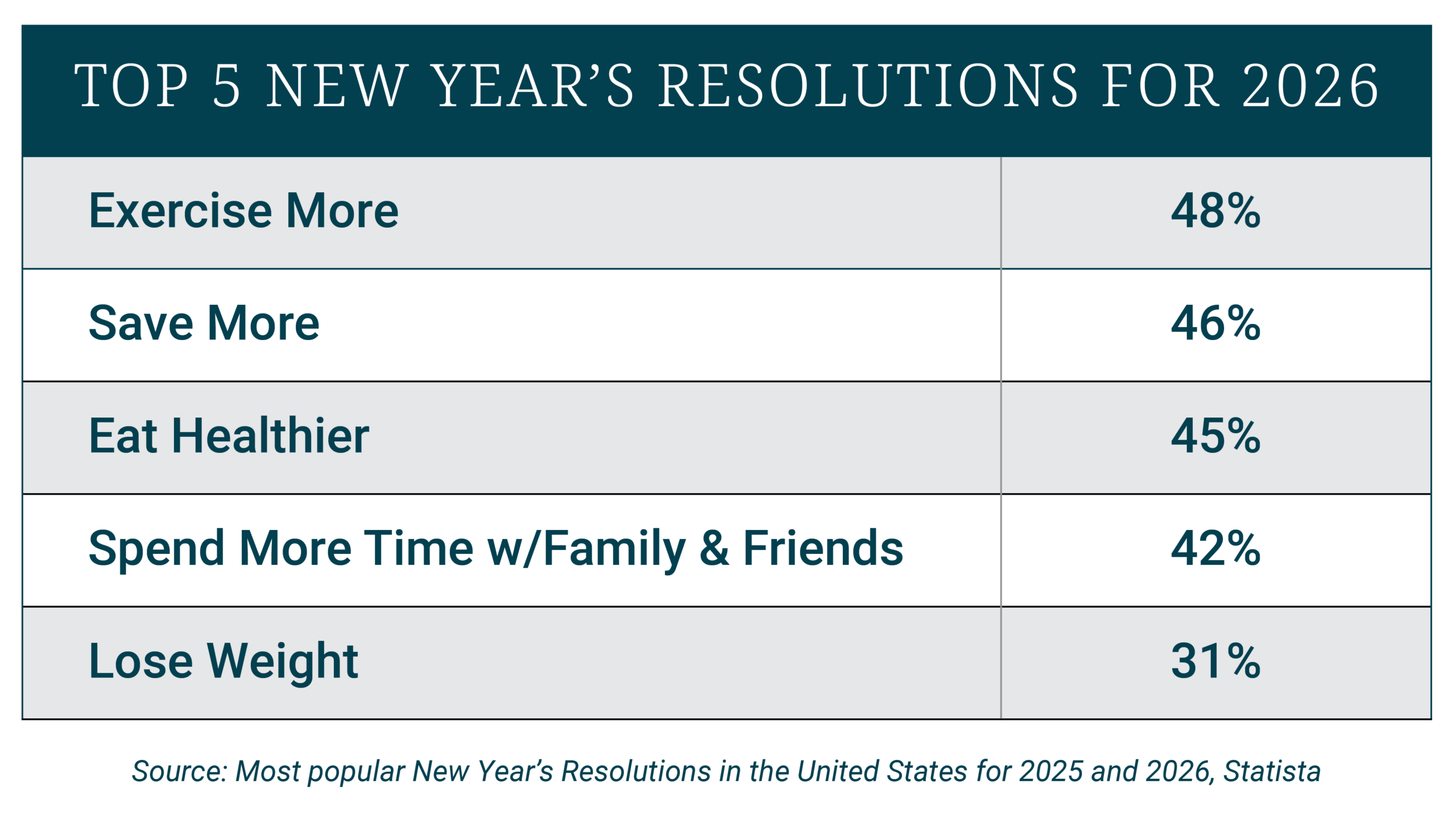

Even for those who do not believe in traditional New Year’s resolutions, the start of a new year naturally brings a sense of renewal. It is a moment that invites reflection and encourages us to think about how we want our lives to look and feel in the months ahead.

Most people focus on improving their physical, financial, and/or emotional well-being. And yet, just a few weeks into January, many give up.

How can you continue following through once the initial excitement fades? Lasting change rarely comes from willpower alone. It is built on clarity, structure, and support. Making and maintaining resolutions is much like setting and achieving financial goals, an approach we understand well at Crestwood Advisors.

Here are five strategies that can help you stick with your plan.

Your goals are important to you, so they’re important to us! Don’t hesitate to contact your Crestwood team for guidance when you’re resolving to change.

If you are not yet a Crestwood client, please contact us. We are here to help.

This document is provided for general informational purposes only by Crestwood Advisors, an investment adviser. Crestwood Advisors does not endorse, sponsor, or promote any of the products or companies listed or mentioned in this material. Any references to specific products or services are purely incidental and are included solely to illustrate potential strategies or concepts. The inclusion of such references does not imply any form of partnership, relationship, or approval by the Firm.

The One Big Beautiful Bill Act (OBBBA) introduces several tax-law changes that significantly affect how the Alternative Minimum Tax (AMT) applies beginning in 2026. While the law keeps the higher AMT exemption amounts originally introduced under the Tax Cuts and Jobs Act (TCJA), it lowers the income thresholds where the exemption begins to phase out and accelerates the phaseout rate once those thresholds are crossed.

Starting in 2026, the exemption’s phaseout thresholds revert to lower levels than under TCJA: $500,000 for single filers, and $1,000,000 for married (joint) filers, before income-based reduction of the exemption. Simultaneously, the phaseout rate doubles, from 25% under TCJA rules to 50% under the OBBBA.

These changes make the AMT more likely to affect higher-income taxpayers and anyone with large AMT “preference items,” most notably, Incentive Stock Option or “ISO” exercises.

The Impact on ISOs

For people with Incentive Stock Options, the AMT impact becomes particularly important. When you exercise an ISO and hold the shares, the “bargain element” (the difference between the stock’s market value at exercise and your strike price) is not regular taxable income, but it is included in AMT income. Under OBBBA’s tightened phaseout thresholds, this AMT add-on can tip many taxpayers into AMT liability—even those who previously avoided it under TCJA’s more generous rules.

In addition, OBBBA modifies the SALT deduction cap, allowing a higher deduction for many taxpayers. But under the AMT system, SALT deductions are added back, meaning a larger SALT deduction can unintentionally contribute to triggering AMT when combined with ISO exercises.

Because of these changes, many ISO holders may face greater AMT exposure beginning in 2026 than they have before.

What to Do

Everybody’s tax situation is different. But if you are in a high tax bracket and have access to ISOs as part of your compensation, you may include the following as part of your tax plan this year:

Model your AMT exposure before exercising ISOs. Consider front-loading ISO exercises this year rather than waiting, if it also makes sense financially and you can afford any cash outlays or holding risks.

Plan your SALT deduction more carefully. If you live in a high-tax state or expect large state and local taxes, combining that with ISO exercises may magnify AMT risk.

Keep in mind your AMT carryforward credit potential. If you do trigger AMT in a year because of timing (e.g., a big ISO exercise), you might be eligible to recover some of the extra AMT paid in future years via the “minimum tax credit.”

Most importantly, check with your financial and tax advisors if you have both ISOs and large itemized deductions. Ignoring or not fully understanding and planning for the changes to the AMT tax regimen in the OBBBA may subject you to significant additional tax exposure.

If you would like to learn more about ISOs, the AMT, and the OBBBA, please reach out to your Crestwood team. If you are not yet working with Crestwood, please contact us to discuss your individual circumstances.

This document is provided for general informational purposes only by Crestwood Advisors, an investment adviser. Crestwood Advisors does not provide legal advice, and this document should not be construed as containing legal advice. For legal advice, consult with a licensed attorney. This document should not be construed as containing tax advice. For tax advice, consult with your tax adviser.

Life rarely follows a straight path. Careers grow and shift; families evolve, and opportunities appear in ways we cannot always predict. Each moment impacts your financial life, which is why a financial plan cannot be something you build once and leave untouched. It must move with you.

At Crestwood, we view planning as an ongoing conversation between two things. The first is the life you are building, with its goals, responsibilities, and turning points. The second is the financial structure that supports it, from investing and cash flow to tax planning and long-term protection. One defines the direction. The other provides the strategies to reach it. Without clarity around your life, the numbers are incomplete. Without thoughtful analysis, your goals remain hopes rather than actions.

Transitions are where planning does its best work.

Every major life change requires decisions. Some come from joyful moments like welcoming a child, buying a home, or earning a promotion. Others arrive through challenges such as illness, a shift in family structure, or a sudden change in your work. And then there are the transitions that bring a layer of complexity that people often do not expect.

For example, when compensation begins to include stock, options, or long-term incentives, you may find yourself managing vesting schedules, taxes, and concentration risk. When you own a business and begin thinking about an eventual sale, there is a long list of choices around structure, timing, valuation, and what life will look like after you step away. When you are approaching retirement, the focus shifts from growing assets to creating reliable income, managing taxes over decades, and building a thoughtful legacy plan.

Though these situations look different on the surface, they all share a common theme: every transition touches your financial life, and each one is easier to navigate with a clear plan.

Planning to Meet your Milestones

Below are the types of life events that often trigger the need for planning.

Marriage

Merging two financial systems is an important moment to align values, review tax considerations, update insurance, and ensure beneficiary and estate planning documents reflect your shared priorities.

Birth or Adoption of a Child

New responsibilities come with new challenges and expectations. Planning for education, guardianship choices, insurance updates, and building long-term financial stability all become part of the conversation.

Buying or Renovating a Home

A home changes your balance sheet and your cash flow. It is helpful to revisit housing costs, mortgage structure, property taxes, and the role real estate plays in your long-term plan.

Career Change

A shift in income, benefits, or equity compensation can affect savings goals and tax planning. Reviewing your budget, emergency fund, and employer-sponsored benefits helps keep your plan on track.

Divorce

This transition often requires redefining financial independence. Asset division, new spending patterns, insurance adjustments, and updated estate planning documents become priorities.

Illness or Disability

Health changes can alter both income and expenses. Planning helps prepare through stronger cash reserves, updated insurance coverage, and thoughtful contingency strategies.

Retirement

Moving from earning to drawing from your assets is one of the most significant transitions in your financial life. A detailed plan can help you understand income sustainability, tax-efficient withdrawal strategies, healthcare considerations, and legacy goals.

Unexpected Windfall or Inheritance

A sudden increase in wealth can create opportunity along with new questions. A structured plan helps address tax implications, investment decisions, and long-term alignment with your goals.

A financial plan is not a document; it is a process that moves with you.

Whether you are navigating equity compensation, preparing for the sale of a business, approaching retirement, or simply entering a new season of life, transitions create the need for good decisions. Planning provides clarity, reduces uncertainty, and helps you act with intention instead of reaction.

As you look ahead to the coming year, think about the changes that may be ahead in your own life. Some will be predictable, and others may arrive unexpectedly. A strong plan can help you prepare for both.

If you would like support updating your financial plan or building one for the first time, your Crestwood team is here to help you move into the next stage with confidence.