January set a tone for a more cautious investor stance. Much of the U.S. was forced to trudge through snow from recent winter storms and similarly labor markets are trudging slowly along. We remain in a low-hire, low-fire equilibrium. Employers are hesitant to expand, given fiscal uncertainty but are equally loath to let go of trained staff.

While corporate earnings are projected to remain healthy, with an estimated 14% growth for the year, the variables of trade policy and central bank transition create a challenging environment.

After three consecutive cuts to end 2025, the Fed shifted stance to a wait-and-see outlook as the committee voted to hold interest rates steady at the January meeting. The FOMC’s internal debate appears centered on the neutral rate (the level at which policy neither stimulates nor restricts growth) with two of the twelve voters advocating for further cuts to support a slowing manufacturing sector.

A notable development was the nomination of Kevin Warsh to succeed Powell when his term ends in May. During his previous time as a Fed Governor (2006-2011), Warsh was initially supportive of crisis-era liquidity and low rates but opposed the second round of quantitative easing (QE2) in 2011 which he believed would lead to inflation.

Warsh has yet to be confirmed, which could be a challenging process1, but understanding his outlook on the Federal Reserve can provide insight to how he might act as Fed Chair.

Warsh In His Own Words

In a November opinion piece in the Wall Street Journal2, Warsh outlined his vision:

“Fundamental reform of monetary and regulatory policy would unlock the benefits of AI to all Americans. The economy would be stronger. Living standards would be higher. Inflation would fall further. And the Fed will have contributed to a new golden age.”

Setting aside the utopian prose, his outlook is reflected in four theses, and we examine each in the context of what they mean for investors.

1) “The Fed should discard its forecast of stagflation in the next couple of years”. He believes that ”AI will be a significant disinflationary force, increasing productivity and bolstering American competitiveness. Productivity improvements should drive significant increase in real take-home wages.”

Translation: The Fed has been driving by looking in the rear-view mirror (backward looking data that shows a slowing economy and sluggish labor market). Future productivity growth and lower inflation from AI isn’t being factored in, so the Fed is being too conservative.

Implications for Investors:

- Warsh’s logic is that AI productivity gains will manifest rapidly, offsetting the potential inflationary risk of lowering rates prematurely. Advances such as the widespread adoption of PCs and the internet have shown that technology that bolsters workers’ productivity has been a boon for economic growth and corporate earnings and helps to lower inflation.

- We remain optimistic about the benefits of AI but believe that companies (and their investors) that adapt to this technology will see benefits long before the economy. While we agree with Warsh that AI is a rising tide, we believe some boats will rise faster than others.

- If Warsh is less concerned about the potential for inflation, he’s more likely to be willing to lower rates independent of how backward-looking economy data is showing. Lower rates would stimulate the economy and encourage assets like small cap stocks and other speculative investments. This could also provide a tailwind for bond investors

2) “Inflation is a choice.”

Translation: Warsh argues that inflation isn’t the product of an overheated economy but rather the result of too much government spending and expansion of the Fed’s balance sheet. The head of the snake (the Fed) would be eating less of its own tail (buying its own debt).

Implications for Investors:

- Warsh favors shrinking the Fed’s balance sheet, which could manifest in a withdrawal of meaningful government buying of Treasurys.

- We agree that excessive government stimulus during the pandemic contributed to a surge in consumer spending and was a major contributor to inflation. However, the Fed’s balance sheet is used for quantitative easing (QE) programs designed to provide liquidity to markets and influence interest rates beyond short-term rates. Considering the U.S. Dollar is used globally for trade, many foreign banks and financial entities that hold U.S. Dollars need consistent access to U.S. debt markets. In periods of market stress, the Fed has used its balance sheet to support the normal functioning of cash and bond markets.

- While shrinking the Fed’s balance sheet is a laudable financial goal, it may prove difficult if long-term rates crimp consumers or periods of financial stress require Fed intervention.

- If this were to occur, it would likely lead to a steepening of the yield curve, which in turn would lead to higher borrowing costs across the economy (mortgages, corporate bonds, etc.). However, higher borrowing costs would slow the economy. Thus, even if the Fed decided to allow the curve to steepen, at a certain point they would be forced to resume purchases. This dichotomy raises doubt (and speculation) about the degree to which the policy might happen.

3) “The Fed’s rules and regulations have systematically disadvantaged small and medium-sized banks, which has slowed the flow of credit”.

Translation: Warsh believes that by easing regulatory requirements for smaller lenders, there will be additional availability of credit.

Implications for Investors:

- Improving the availability of credit would help grease the wheels of the U.S. economy by encouraging lending. Smaller banks would have more ability to lend, which could benefit smaller businesses.

- However, the benefits of this could be muted in the context of an environment where credit is available, but at higher rates. For example, a lender might be willing to offer a larger mortgage but at a higher rate of interest.

- This could lead to real estate prices continuing to remain high.

3) “Fed leaders have tried to bind U.S. banks to a complicated, vaunted set of rules in the name of global regulatory convergence.”

Translation:

Warsh argues that the Fed should seek to deregulate U.S. banks and encourage them to de-couple rather than coordinate with their overseas counterparts.

Implications for Investors:

- Deregulation of banks, in general, would likely lead to increased lending and profitability and therefore higher prices on bank stocks.

- Many of the current regulations sprang out of past financial crises and were structured to try to prevent history from repeating. Often a crisis may start locally but have global implications. Notable examples like the 2008 Global Financial Crisis, the Great Depression, the Savings and Loan Crisis of the 1980’s-90’s, etc.

- While excess regulation acts as a speed bump on the road to revenue, a lack of speed limits and guardrails wouldn’t make banks better “drivers”. It would likely result in banks using greater financial leverage, reducing loan quality and potentially repeating some of the errors that led to the Global Financial Crisis.

Capital Markets

Equity markets saw a notable rotation in January as investors grew cautious of the AI theme driving market recent gains amidst higher valuations. Notably this led to a wider breadth of stocks driving market gains including smaller companies (as measured by the Russell 2000).

Official data reported in January remains cloudy due to the late-2025 government shutdown. This data lag created a volatility vacuum where anecdotal evidence and earnings calls carried more weight than usual as earnings were released.

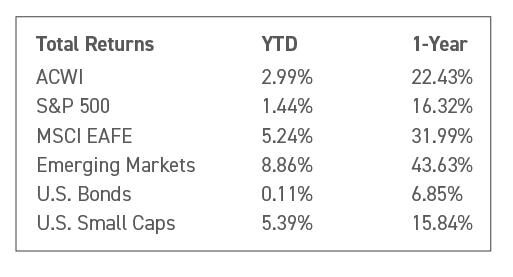

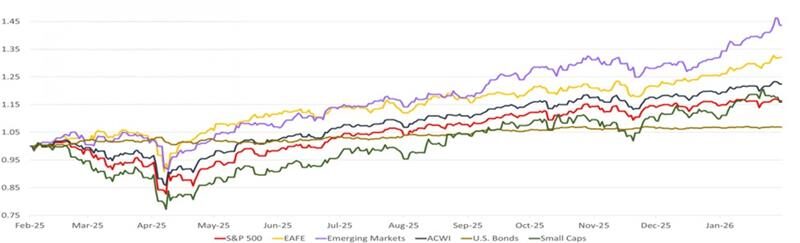

Emerging Market Equities lead the way returning an impressive 8.9% for the month. U.S. Small Caps (Russell 2000) and Developed International Equities (MSCI EAFE) also showed large gains, returning 5.4% and 5.2% respectively. U.S. Large Caps (S&P 500) lagged, returning 1.44% in January. Bonds, as measured by Bloomberg’s U.S. Aggregate index, were nearly flat for another month, eking out a slightly positive 0.11%.

Return of Market Indices

2025 was a year of economic uncertainty and concern, but also of resilience and growth. In this month’s Economic Update, we look back at the issues that dominated our thinking on the economy and financial markets each quarter and then look forward to what we’re focused on in 2026.

Source: Bloomberg. EAFE is MSCI EAFE Index(1), Emerging Markets is MSCI Emerging Markets(2) and U.S. Bonds is Barclays U.S. Aggregate(3). ACWI is the MSCI ACWI Index(4). Small Caps is the Russell 2000 Index(5). S&P 500 is the S&P 500 Index(6). The above information is as of 1/31/2026.

1 Warsh’s journey to become Fed Chair is unlikely to be quick. Post-nomination, the next step toward approval is for vetting to go through the Senate Banking Committee. However, committee member Senator Thom Tillis (R-NC) has indicated he would not on any Fed nominee until the Department of Justice’s investigation of Chair Powell over the Fed’s headquarters is resolved which he believes is politically motivated Senator Tillis’ term ends in 2026, and he is not seeking re-election, making him less susceptible to political pressure. The Senate Banking Committee is narrowly divided (13 Republicans to 11 Democrats), thus if Tillis refuses to support the nominee, the committee the nomination could stall.

2 Warsh, Kevin The Federal Reserve’s Broken Leadership, Wall Street Journal Opinion 11/16/25

This document contains forward-looking statements, predictions and forecasts (“forward-looking statements”) concerning our beliefs and opinions in respect of the future. Forward-looking statements necessarily involve risks and uncertainties, and undue reliance should not be placed on them. There can be no assurance that forward-looking statements will prove to be accurate, and actual results and future events could differ materially from those anticipated in such statements.